Local clay for pottery and ‘one-stop shop’ for pottery supplies

Background

The number of potters in Oman in 2018 was 1196, with PACI members producing 39,800 pieces of pottery. From an estimated 592 metric tonnes of clay. Further local research is required to confirm clay usage.

The main two techniques for manufacturing the pieces of pottery are:

- Bespoke – made by hand often using a potter’s wheel, these pieces are time and labour intensive and tend to be for traditional Omani pottery.

- Moulded – with Jigger Jolly process being used for symmetrical shapes whilst the slip casting process, allows for mass production of repeatable quality pieces specifically non symmetrical shapes and features.

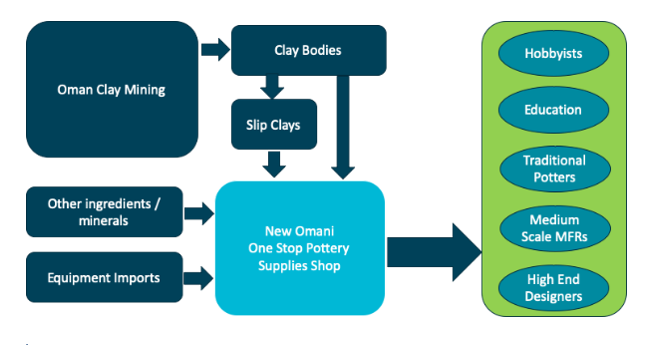

As a benchmark we have used Potclays, a UK-based company who have positioned themselves as a ‘one-stop-shop’ for potters. Their operations include refining and sale of 50-60 tonnes of pottery clays a week and retail of a wide range of equipment and consumables for hobbyists and small-scale commercial potters. Figure below provides an overview of how the Potclays structure could be applied to the Omani context. As a rule of thumb wholesale prices are a twenty percent reduction from the listed selling price for clay.

As a benchmark we have used Potclays, a UK-based company who have positioned themselves as a ‘one-stop-shop’ for potters. Their operations include refining and sale of 50-60 tonnes of pottery clays a week and retail of a wide range of equipment and consumables for hobbyists and small-scale commercial potters. Figure below provides an overview of how the Potclays structure could be applied to the Omani context. As a rule of thumb wholesale prices are a twenty percent reduction from the listed selling price for clay.

Figure 75

The original purpose of this project had been to investigate the opportunity for clay production only. Further research is needed to gain an understanding of the opportunity for retail of equipment, other supplies and consumables. This will be time dependent, influenced by the growth of the other opportunities within this sector.

[/expand]

About the market for local clay in Oman

Globally, hobbyist pottery creation is increasing due to the rise of maker-based content and communities on sites like YouTube. The ability to source materials, tools and equipment via online retailers is enabling people around the world to learn at home or in small groups.

This trend is applicable to Oman and we believe that the number of potters will increase in the next few years, providing a market for locally produced clays, a proportion of which may be mined in Oman. Potclays has seen increases in year on year sales of 15% year for the last 5 years.

Slip casting clays come in various types dependant on the final product, such as variations of, Terracotta, Stoneware, Porcelain and Earthenware. Soda ash and Sodium Silicate are mixed with the base clay to create the correct recipe for the slip clay needed for the end application

Estimates based on Potclays sales is OMR 100-350 per tonne for bulk pallet sales (wholesale), and OMR 0.9 –1.5 per kg in bag form for direct retail sales.

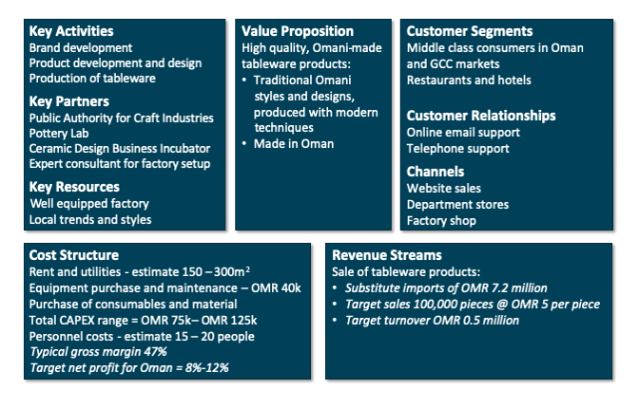

Further research is needed to profile current and forecast demand within the sultanate. It is assumed that a facility of the size of Potclays is a good match to support the likely growth of demand in the sector. The assumption is therefore sales of OMR 190k pa for clay only. Excess capacity is assumed to be exported, primarily to the GCC region. Further research at the business plan stage should consider the growth profile of demand and matching this with the capacity development.

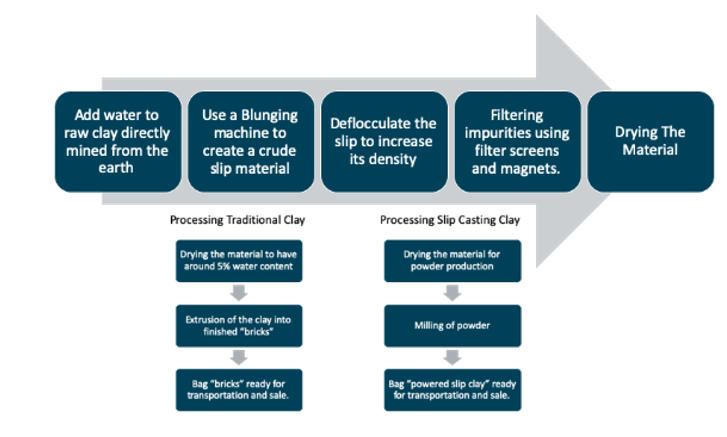

Typical facilities for clay production

The types of clay likely to be required by Omani potters follow the basic process outlined below in Figure .

Figure 76

The Potclays factory runs three separate lines to enable production of 50 – 60 tonnes a week of different types of clay concurrently, reducing the need to wash out and clean the full production line. Each production line consists of blunging, deflocculating, filtering, drying machinery and pugmills required to produce both traditional ready to use clay and slip casting clays. We estimate that this provides a capacity of around 2,500 MTpa

Figure 77

The location of the clay processing plant will depend on a number of factors related to the number of active clay mines and their location. It may be cost effective to process the material in a facility setup at the mining site or transport raw materials from a number of mines for processing a facility located close to the end users.

Operating costs include:

- Energy – Total plant estimated at 500kW

- Water – 3000 litres / day

- Labour – 1 manager, 1 production supervisor, 2 fitters & 8 workers

Potclays have suggested that a greenfield site to replicate their facility with new equipment would cost up to OMR 500k – although this is for a capacity significantly higher than current Omani demand.

There is an open question as to how the investment profile build up over time.

Initial investment is therefore may be half of the total amount, which may also be reduced by the use of used or refurbished equipment.

Canvas

Figure 78

The industry expectation for a clay production facility would be a net profit level of 5-10% in the UK, but for Oman is likely to be 8-12% due to lower labour and energy costs. Further research is needed to establish the depreciation assumptions to understand the return on investment profile and payback period – which is expected to be 2-4 years, depending upon the ramp up of sales, and initial installed capacity.

Further Information

This page provides an introduction and overview of the nature of the selected opportunity. For more detailed information or to get involved with this opportunity, please contact IIC: info@iic.om