Reducing energy costs for chromite ore processing

Background

The primary added value application of chromite is in the production of ferrochrome. To produce ferrochrome, chromite ore must complete several stages of energy intensive processing. The most energy intensive step is the smelting activity. This involves a carbothermic reduction process conducted at temperatures often in excess of 1600°C that is typically conducted using a submerged arc furnace.

Figure ‑6. Submerged arc furnace for chromium smelting in Oman (source:ATIFC).

During primary research interviews as well as the workshops completed in July 2021, participants stated that high energy costs were limiting their competitiveness in international ferrochrome markets. Through earlier scouting activities, ferrochrome producers in Oman have reported energy consumptions of 4 – 5 MWh per tonne of ferrochrome produced. International benchmarks suggest that energy consumption in the region of 2.4 – 3.5 MWh per tonne of ferrochrome is possible with the latest processing technologies and process management1,2. Whilst there are many factors that can impact energy consumption that make international comparisons difficult, there does appear to be an opportunity to reduce energy consumption in chromite ore processing.

In this section, two approaches to reducing energy costs are explored: policy options and technical options. Section 0 provides recommendations on how elements from these two approaches could be combined to help reduce energy costs in the short term and in the long term.

Policy options

Provide special energy tariffs for chromite processing companies

Many other chromite-producing countries have struggled to develop appropriate energy policies to encourage added value chromite ore processing. Zimbabwe, which has the second highest chromite reserves after South Africa, has experimented with various policy measures in an effort to encourage domestic chromite ore smelting. These have included the introduction of a 20% tax on chromite ore exports and a complete ban on chromite ore exports in 2015. However, this did not lead to the expected increase in ferrochrome production due to:

-

Lack of investment in modern smelting technology

-

Falling ferrochrome prices in international markets

-

High electricity tariffs.

In 2015, Zimbabwe changed its policy in favour of reinitiating chromite ore exports whilst also providing a reduction in electricity tariffs to benefit ferrochrome producers. The new policy measures included1:

-

Allowing chromite ore exports of 30 million tonnes of chromite ore over and above the export of processed ferrochrome.

-

Increase of chromite ore royalties from 2% to 5%.

-

Reduction of the electricity tariff from 8.00 US cents per kWh to 6.7 US cents per kWh.

Despite reductions in energy tariffs being regular proposed as a solution to rising energy costs for ferrochrome producers, this example from Zimbabwe is the only documented example identified of this type of policy being implemented. No detailed explanation of why this type of policy to support reduced energy tariffs has not been more widely adopted has been identified but arguments against this approach include the following:

-

Introducing subsidised energy tariffs may reduce private investment in R&D and new capital equipment in order to improve energy efficiency.

-

Once introduced, subsidised energy tariffs are difficult to remove without impacting the competitiveness of the industry.

-

From a national economy perspective, it may be preferable to allow the producers with the cost structure to cease production in order to enable the producers with the lowest cost structure to grow and gain further ‘economies of scale’ benefits.

-

Providing subsidised energy tariffs for industrial users will benefit the most energy intensive industries the most. This would run contrary to the industrial strategy of many countries, including China, that are trying to reorientate their manufacturing base towards energy efficiency and overall reductions in energy consumption.

Introduce an export duty on chromite ore exports

Whilst introducing an export duty on chrome exports would not help to reduce the energy costs of Omani ferrochrome producers, this type of policy measure has been used by other countries facing reduced competitiveness due to high electricity costs.

In South Africa, a 500% increase in electricity costs since 2008 has seen around 40% of the ferrochrome production capacity closed due to reduced competitiveness in the international market. This has prompted the government to propose an export tax on chromite ore. This suggestion has been welcomed by ferrochrome producers, who believe that it would lead to an increase in the production costs of ferrochrome producers in China (who import 84% of their chromite ore supply from South Africa), which would in turn make South African ferrochrome prices more competitive. However, the proposed export duty has been fiercely rejected by the unintegrated chrome mining companies, who fear that it could lead to a 22-32% reduction in global market share for South African chromite ore exporters1. ChromeSA, the trade organisation representing unintegrated chromite mining companies in South Africa, has suggested that favourable energy tariffs should be provided to ferrochrome producers instead of imposing the ore export tax.

Zimbabwe has recently reintroduced the ban on chromite ore exports due to insufficient suppliers to feed the 22 smelters now operating in the country2.

India has for a number of years imposed a 30% export duty on chromite ore3. This duty was briefly lifted for the 2016-17 budget but then re-imposed due to complaints by ferrochrome producers about a lack of local chromite ore supply4. It is claimed that the chromite ore export duty has resulted in an increased tax base, higher investment in the industry, benefits to the local communities and skills development.

It is suggested that imposing an export duty on chromite ore may be an appropriate option if:

-

there is insufficient domestic supply of chromite ore to feed the available ferrochrome production capacity; and,

-

there is sufficient electricity generation capacity to reliably power the available ferrochrome production capacity.

In Oman, ferrochrome producers have reported that there is insufficient domestic supply of chromite ore, which has forced them to import ore at international prices. The issue of chromite ore availability was also cited in an issue in the closure of the ferrochrome plant previously operated by Gulf Mining Group.

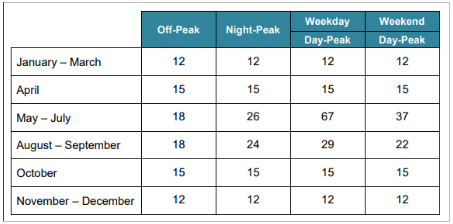

It is not clear if there is sufficient electricity generation capacity to support increased ferrochrome production as there are already challenges in supplying electricity during the summer time due to the very high nationwide demand for electricity for air conditioning and ventilation applications at these times. This is reflected in the 550% increase in the electricity tariffs for industrial users during peak hours of the summer months compared to winter months – as shown in Table 26‑1.

Table-6. Bulk Supply Tariffs for ‘MIS’ network in OMR/MWh (source: Authority for Public Services Regulation).

There are therefore arguments for and against the introduction of an export duty on chromite ore in Oman. However, it is suggested that this policy measure should be investigated as a potential short-term solution to enhance the competitiveness of Omani ferrochrome producers. The impact of such a policy on smaller scale chromite ore producers should be investigated as part of this evaluation.

Further develop renewable energy sources

Having seen significant rises in the cost of electricity, the South African ferrochrome production industry is planning large scale investments in self-generation in order to reduce their energy costs. 750 MW of renewable and co-generated electricity production capacity is planned by 20241. This has been facilitated by changes in government policy to raise the licensing-exemption threshold for private companies to produce their own electricity from 1 MW to 100 MW2.

In Oman, the potential for renewable energy to address the energy challenges faced by ferrochrome producers has already been recognised. In early 2021, Qabas, the renewable energy arm of Shell Oman, completed a 25 MW solar electricity farm at Sohar Freezone3. One of the beneficiaries of this renewable electricity is Al Tamman Indsil Ferro Chrome.

Figure‑7. Qabas solar electricity farm – Sohar Freezone.

The cost of utility scale photovoltaic systems continues to decline, with costs dipping below $1 per MW in the USA according to National Renewable Energy Laboratory1. Furthermore, the Public Authority of Special Economic Zones and Free Zones has plans to implement a total of 1 GW of solar PV installations in Sohar2.

With some of the best ‘solar resources’ of any country, Oman has a unique opportunity to turn the challenge of high energy prices into a strategic and sustainable competitive advantage through the adoption of renewable energy technologies. The added advantage of utilising renewable energy for ferrochrome smelting is that it will significantly reduce the overall carbon footprint of the final product. For example, it is estimated that, by displacing natural gas-fired power generation, the Qabas solar electricity farm will avoid 25,000 tonnes of CO2 emissions annually. This may well be of interest to downstream industries, such as the automotive or construction sectors, that are working towards carbon footprint reduction goals. Whilst a low carbon footprint ferrochrome product may not attract a price premium at this time, it would offer a point of differentiation for Omani ferrochrome producers in what is a very competitive market.

Allow the price of fossil fuels to increase

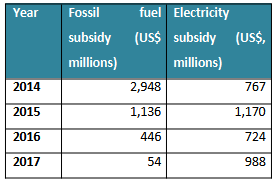

Historically, gas and electricity costs in Oman have been subsidised by the government. Since 2015, there has been a strategic effort to reduce these subsidies – see Table 26‑2. The objectives of this policy change were to reduce the burden on the national budget and also to encourage industry investment in energy efficiency measures.

Table‑7. Estimated cost of subsidies provided by the government of Oman for fossil fuels and electricity (source: Amann et al., 2021).

It may appear counterintuitive, but one policy option to address the challenge of poor competitivity of the chrome processing industry might be to allow the cost of energy inputs to increase. This idea is based on the ‘Porter Hypothesis’ which suggests that imposing strict environmental standards on an industry ultimately leads to improve competitiveness as they stimulate innovation that more than offset any costs incurred by the industry to comply with the new standards.

There is evidence that the Porter Hypothesis1 is valid in Omani industry. Based on analysis of data from the Omani Annual Industrial Survey from 2012 and 2017, Amman et al. (2021), found that increases in fossil fuel prices actually led to improvements in the competitiveness of industrial companies. The authors suggest that this improvement in productivity was achieved through greater investment in new, more efficient production technologies, investment in control systems to enable better energy management as well as improvements in labour productivity. However, increases in electricity prices did not result in the same improvements and had some negative impacts on overall competitiveness. This is important as although coke and natural gas are used in the ferrochrome smelting process, the majority of the energy input for submerged arc furnace smelting comes from electricity.

This programme has not been able to obtain any data concerning the level of fossil fuel subsidies in Oman since 2017 and so it is not clear if the trend of reducing fossil fuel subsidies has continued. Assuming that is has, the level of subsidies is likely to be close to zero by late 2021. Based on the Porter Hypothesis, the next logical step might therefore be to begin imposing taxes on fossil fuels to increase prices further. To ensure that such measures continue to deliver improvements in overall competitiveness, the government revenue from this tax could be ringfenced and used to support activities targeted at improving energy efficiency in industry (e.g., R&D activities, investment in new production technologies and improved control systems, enhanced training for production workers etc.). Examples of some of the technical options to reduce energy consumption and costs that the chrome processing industry might wish to invest in (with support from are presented in the following section