Introduction

The MENA region, including Oman, has several advantages for glass manufacture. As well as potential supplies of key raw materials (silica sand and soda ash), Oman benefits from a continuous supply of clean and cheap power, relatively low fuel costs which lead to lower transportation costs, and a location that is well suited for exports to potential large markets such as India1.

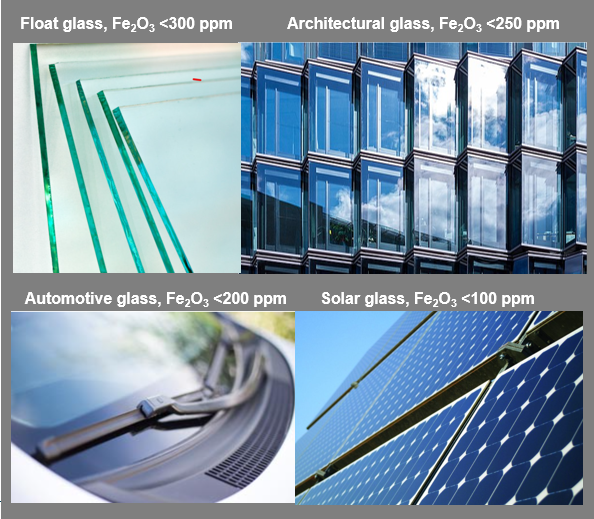

The major categories in the glass market are container glass and float glass. Oman is currently manufacturing only container glass (through the operations of Pragati Glass and Majan Glass). There are no float glass manufacturers in Oman, although there are some trading companies such as Al Tasnim Enterprises, which has recently established a glass processing division that adds value to float glass through activities such as tempering2. However, float glass is worth consideration as a potential market opportunity for Oman. The largest end applications of float glass are construction and automotive applications. Solar glass is a relatively small application of float glass but is considered as a separate category in this section because it has additional purity requirements but has very high growth potential and is an obvious future opportunity for Oman. Table 16‑1 provides an indicative guide to the purity of silica sand required for the manufacture of different types of glass.

Table 16‑1. Indicative guide to silica sand purity for different categories of glass

|

Application |

Silica content |

Fe2O3 content |

Al2O3 content |

Other limits |

Particle size and morphology |

|

Colourless container glass1 |

98.5-99% |

<0.035% |

<0.5% |

Limits on Na2O, K2O, colorants (Ni, Cu, Co), refractory minerals |

0.1-0.6 mm Angular grains may aid melting |

|

Coloured container glass |

0.25-0.3% |

0.2-1.6% |

|||

|

Float glass |

0.04 – 0.1% |

0.03% |

|||

|

Solar glass2 |

>99.7% |

0.0075% |

0.08% |

Container glass

Container glass is used to make bottles or containers for packaging of food, beverage, and pharmaceuticals/technical products. In the Middle East, these three applications account for about 56%, 29%, and 15% of container glass total tonnage respectively1.

Container glass market

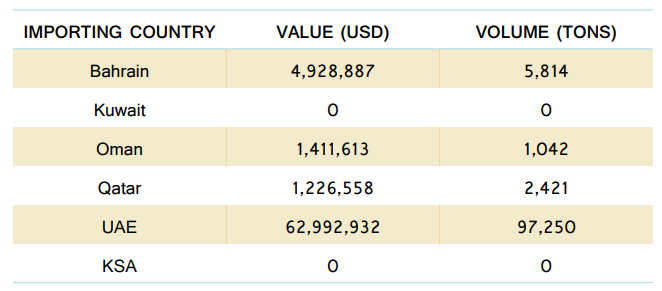

As of 2017, the volume of glass bottles and containers in this region was estimated to be 20,951 million units, predicted to grow at a CAGR of 4.13% to 2023, to reach a volume of 26,694 million units. A separate source estimates that the region had a shortage of glass containers of approximately 300,000 tons in 2017. The growth in use of container glass across the Middle East is driven by increasing disposable income and by rising popularity of glass in premium packaging and consumer goods. For example, glass is perceived to offer health and environmental benefits, and its potential for recycling is leading to a slowly rising demand for glass over polypropylene. Growing demand in the pharmaceutical industry in the Middle East is also expected to contribute to demand for container glass: for example, Pfizer in Saudi Arabia recently invested over USD 50 million for a solid dose manufacturing facility for production and packaging, driving the demand for glass bottles and containers1. Table 16‑2 shows that Oman imported container glass to a value of over $1 million in 2017, though this is dwarfed by UAE with imports of almost $63 million.

Table 16‑2. Imports of container glass in GCC countries, 2017328

Container glass production in Oman

Currently, container glass in Oman is manufactured by Majan Glass (production capacity 250 metric tons per day1) and by Pragati Glass (production capacity of Omani plant 135 tons per day2). Majan Glass supplies glass containers from 88 ml to 1250 ml in flint, green, and amber, and in various sizes, for carbonated soft drinks, juices, food products, malt beverages, etc. Pragati Glass produces glass bottles in Oman and has an Indian plant with a capacity of 170 tons per day. These companies rely on imported silica sand because of lack of local production. Pragati Glass imports silica sand mainly from Saudi Arabia, Egypt, and Jordan3 and Majan Glass imports silica sand mainly from Saudi Arabia, with some supplies from Egypt and India (India was an important supplier during the pandemic as its ports remained open)4.

Saudi Arabia is the cheapest source because the sand can be transported by truck. The trucks can be loaded with other goods on return trips back to Saudi via UAE, which further reduces transport costs. However, Pragati Glass view the reliance on Saudi sand as a risk: Saudi sand is a valuable natural resource, for which supplies are finite, and Saudi Arabia could decide to stop exporting supplies. Currently, the most economic alternative is Indian sources, but this is less economically attractive because shipping is required, and loose sand is difficult to transport in shipping containers. A local supply of silica sand would improve the security of raw material supplies and would strengthen Pragati Glass and Oman’s glassmaking industry.

Majan Glass is in the preliminary stages of exploring local supplies of silica sand from a source near Duqm, working collaboratively with MDO. They have completed primary drilling tests and are working with an external testing lab in the UK to evaluate the sand. Preliminary results are encouraging, with no difference between Omani sand and Saudi sand in melting tests. The next step is to establish if the sample is representative of the larger supply, so they are currently engaged in drilling to a depth of 8 to 10 metres to evaluate the sand further. The initial samples are of a purity of 96% to 98% silica, so some small level of beneficiation is required, and Majan Glass is engaging with three possible partners for beneficiation.

The market data discussed here suggest an unmet need for container glass in Oman and in potential export markets across the MENA region, suggesting an opportunity to increase the manufacturing of container glass in Oman. Discussions with Pragati Glass and Majan Glass emphasize that establishing a local supply of silica sand would provide economic benefits and greater security for their operations.

Float glass (flat glass)

Production

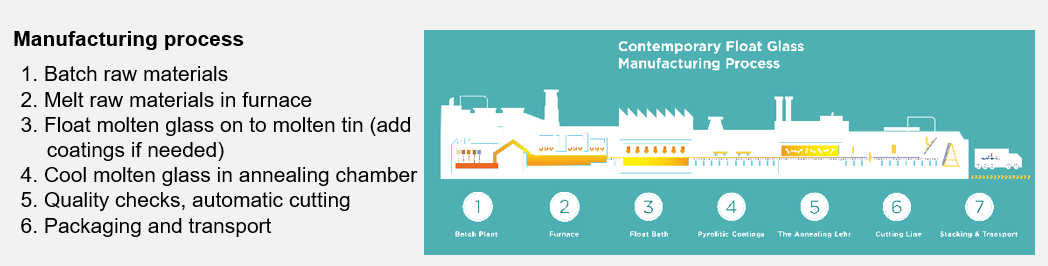

Float glass (or flat glass) is made by pouring molten glass from a furnace into a chamber on to a bed of molten tin in a carefully controlled atmosphere (sometimes called the Pilkington Process)1. The glass floats on the tin and forms itself in the shape of the container. From the chamber, the glass is annealed, meaning that it is cooled at a specific rate to relieve the glass of internal stresses. It emerges at room temperature as a continuous ribbon that can be cut, drilled, machined, edged, bent, and polished. The process is summarized in Figure 16‑1.

Glass produced by the float process can be clear or tinted. Most float glass is clear, i.e. transparent and colourless, and depending on its thickness, it allows 75-92% of visible light to pass through it. Tinted glass (also called heat absorbing glass) is made by adding colouring agents to the batch mix to yield bronze, grey, green, and blue colours.

Annealed float glass can also be used as a base product for production of more advanced glass types2. These include tempered or toughened glass (where the cooling process is manipulated to yield glass that is four to five times stronger than ordinary annealed glass) and laminated glass, where layering can offer safety and security advantages. Major types of float glass, with indication of purity levels of sand needed for its production, are illustrated in Figure 16‑2.

Figure 16‑1. Float glass manufacturing process at Saint Gobain, France1

Float glass market

The global float glass market was valued at $100 billion in 2018 and is projected to grow at a CAGR of approximately 7% through 20291. A similar growth estimate is made for the Middle East and African float or flat glass market (CAGR of over 6% to 2025)2. East Asia is expected to be a prominent regional market for float glass because of growth in construction, automotive, and solar sectors, especially in China.

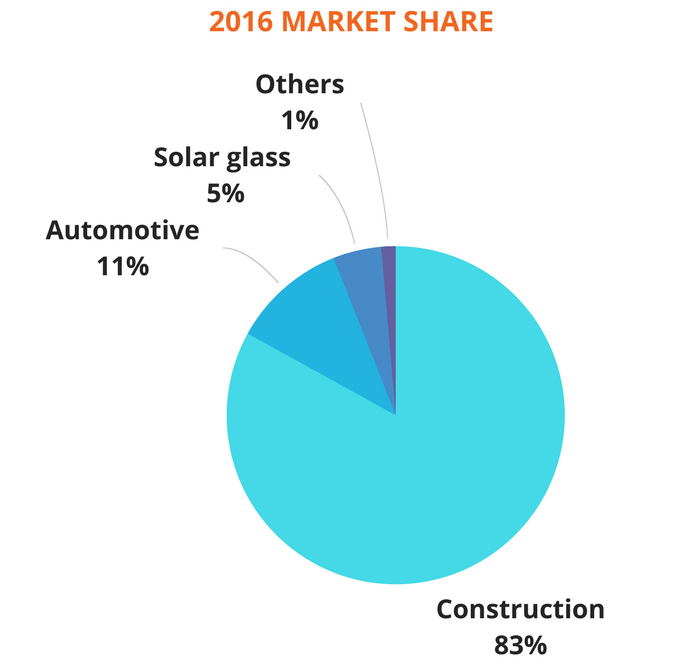

Figure 16‑3 shows the market share of float glass by end application3. The dominant downstream industry globally is construction. The term ‘architectural glass’ is also used for some construction glass, and for any glass used as part of the design in residential or commercial buildings. Automotive applications are the second largest segment. Other categories are solar glass, electronics glass, and mirrors4. In the MENA region, construction activities are expected to drive market demand for float glass, especially driven by initiatives to shift reliance from hydrocarbon-based economies. Growth is also expected to be driven by growth in the automotive industry, either as original equipment supplied to manufacturers of new vehicles, or as automotive glass replacement products supplied for repairs.

Saudi Arabia has recognised an investment opportunity in the float glass industry and is seeking investment to establish a float glass processing plant for the manufacture of specialist glass (safety glass, laminated safety glass, and insulating glass products) from flat sheet glass5. This is expected to require an investment of $50 million to establish a plant of 42 ktpa capacity, with expected IRR of 13% and a payback period of 9.1 years. This provides an example of the diversity of products that can be manufactured from float glass. The proposal states that demand for such glass is expected to increase due to increase in building and construction, consumer goods, automotive, and solar panel sectors

Figure 16‑3. Market share of float glass by industry sector.

Float glass production in Oman

There is no production of float glass in Oman. Currently the potential economic benefits are not high enough for float glass production to be established, but Majan Glass would be keen to develop float glass manufacturing in the future. To be feasible, investment is needed, as well as growth of the necessary technological know-how in Oman. Float glass production is therefore currently a longer term opportunity for Oman.

Solar glass

Introduction

Solar glass is a specialist glass used in both photovoltaic (PV) and in concentrating solar power (CSP) systems. Photovoltaic (PV) systems convert sunlight directly to electricity using PV cells made of semiconductor materials, with cells connected and laminated under tough, high-transmission glass1. CSP systems use reflective devices such as troughs or mirror panels to concentrate sunlight on to a heat transfer material which generates electricity through a turbine, or on to a very high-performance photovoltaic cell that converts heat into electricity. Sand for solar glass must be very low in iron, less than 85 ppm of iron oxide, which is lower than for most float glass2.

Solar glass markets

Both PV and CSP markets still represent a small fraction of the float glass market. However, ongoing investment into solar panels and renewable energy, especially in the UK, US, China, and Japan, means that this sector is expected to grow rapidly. Solar power is also an obvious fit for Oman.

The global solar photovoltaic glass market was valued at $4.5 billion in 2018 and is projected to reach $37.6 billion by 2026, growing at a CAGR of 30.3% from 2019 to 20261. The global concentrated solar power market size was valued at USD 4.5 billion in 2019 and is expected to grow at a compound annual growth rate (CAGR) of 9.7% from 2020 to 20272. Both markets are driven by concerns over carbon emissions. The CSP market is predicted to grow more slowly than the PV market because CSP technology is highly capital-intensive. This is predicted to limit its adoption unless it is supported by governments through regulatory drives.

Solar glass in Oman

There is currently no production of solar glass in Oman. As a higher value product, production of solar glass should be considered as a longer term opportunity once manufacture of float glass is established in the Sultanate.

Case studies

Glass factories in Ma’an, Jordan

Ma’an Development Company was established to work on promoting and marketing Ma’an in Jordan as an industrial area, aiming to raise living standards in Ma’an and South Jordan. As part of this effort, investment is sought to establish both float and container glass factories. These projects will benefit from ready access to high quality silica sand in Jordan, and will produce container glass for various industries float glass for construction, automotive, and potentially for solar glass.

-

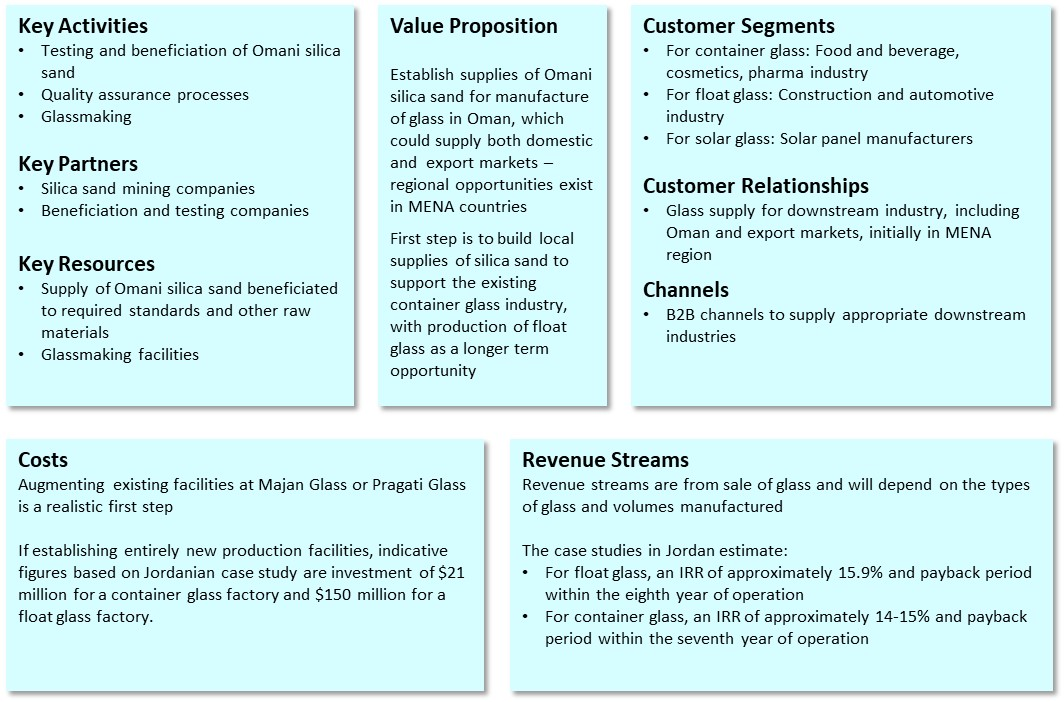

The container glass project is estimated to require a capital investment of $21 million. The IRR for the project is estimated to be approximately 14-15% and the payback period is expected to be within the seventh year of full operation1.

-

The float glass project is estimated to require a capital investment of $150 million. The IRR for the project is estimated to be approximately 15.9% and the payback period is expected to be within the eighth year of full operation2.

Float glass factory in Iran, 2018351

Approximately 500,000 m2 of float glass is produced in Iran each day, with 40% of production exported to the Persian Gulf, Central Asia, and Europe. Iran has ten glass factories, seven of which produce float glass, with capacity of approximately 1.2 million tons.

Iran explored the potential of establishing a float glass factory in Maku Free Zone. Advantages are:

-

Low production costs in Iran because of low energy cost and proximity to raw materials (silica mines with capacity of 6 million tons)

-

Strong regional export markets – demand especially high from Turkey and Iraq, with potential markets suggested in Afghanistan, Pakistan, Oman, and Georgia

-

Ease of doing business in Maku Free Zone – 20-year tax exemption, visa-free region, 100% ownership for foreign investors, unlimited currency exchange to other Free Zones, customs duties exemptions, easy company registration, and free access to investment capital transfer

Table 16‑3 summarises the predicted investment for a float glass factory in Maku Free Zone producing 150,000 tons of float glass annually.

Table 16‑3. Summary of investment required to establish a float glass factory in Maku Free Zone, Iran (currency converted from Iranian Rial to USD using online currency converter)1.

|

Investment |

Fixed investment costs |

USD 84,000,000 |

|

Pre-production expenditure |

USD 24,000 |

|

|

Working capital |

USD 7,380,000 |

|

|

Construction interest expense |

USD 12,090,000 |

|

|

Total investment costs |

USD 103,490,000 |

|

|

Sources of finance |

Equity shares |

USD 24,210,000 |

|

Long-term loan |

USD 67,200,000 |

|

|

Construction interest expense |

USD 12,090,000 |

|

|

Interest |

18% |

|

|

Period of repayment |

5 years |

|

|

Construction period |

12 months |

|

|

Business results |

Net present value of total capital invested at 18% |

USD 26,370,000 |

|

Internal rate of return on investment (IRR) |

23.38% |

|

|

Normal payback |

5.48 years (2023) |

|

|

Net profit at reference year |

17,180,000 |

|

|

Breakeven ratio (%) |

38.66% |

|

|

Labour |

120 people |

Business canvas

Figure 16‑4. Business canvas for establishing a supply of Omani silica sand to support glassmaking in the Sultanate

Next steps

Market demand for many types of glass is strong and predicted to grow, both across the MENA region and globally. Oman’s glassmaking industry is small and the lack of Omani silica sand means the local companies must rely on imported raw materials. Establishing a local supply of silica sand of known specifications would help to grow Omani glassmaking industries and the downstream industries they serve.

Next steps for Oman are:

-

Characterize silica sand deposits and establish reserves sufficient to justify setting up a beneficiation plant and supplying a glass factory. Ensure adequate supply of other raw materials for glassmaking such as soda ash.

-

Conduct a market study to determine the feasibility of establishing a supply of Omani glass and to decide on the type of glass to be supplied. In the first instance this is likely to be a supply of container glass. Building facilities to manufacture float glass and solar glass are likely to be longer term opportunities for Oman.

-

Seek and attract investment and the technical know-how to be able to establish a beneficiation plant that can beneficiate sand to the purity required for the downstream industry of choice (see Section 15).

-

Seek and attract investment to expand the glassmaking facilities of existing Omani manufacturers (Pragati Glass and Majan Glass). The likely initial focus is to expand container glass production but expanding into float glass should be considered.