Background

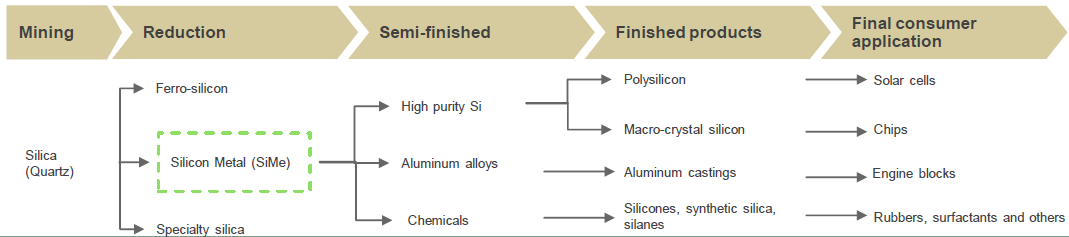

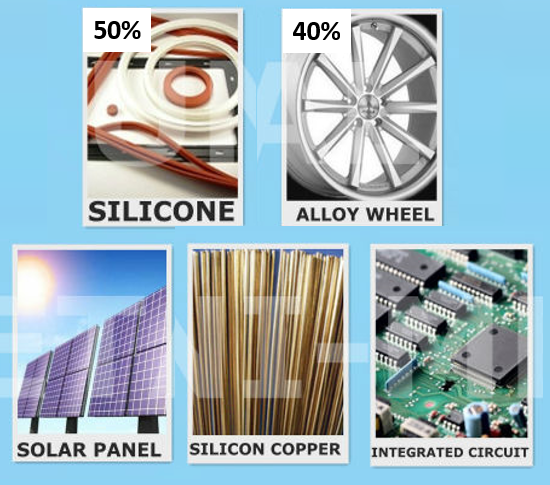

Silicon metal (illustrated in Figure 18‑1) can be produced from quartzite rock through chemical reduction of silica (SiO2) to elemental metallurgical grade silicon (Si). Table 18‑1 shows the approximate proportion of the silicon metal market used for the major downstream applications, with brief comments about the production route1. Figure 18‑2 shows an overview of the silicon metal value chain and Figure 18‑3 illustrates some applications of silicon metal.

Figure 18‑1. Silicon metal

Table 18‑1. Main uses of silicon metal

|

Industry |

Proportion of silicon metal market |

Production |

|

Aluminium alloys |

40% |

Direct use of silicon metal as alloying agent in production of aluminium |

|

Silicones |

50% |

Produced from metallurgical grade silicon, via dimethyldichlorosilane; filler in sealants and lubricants |

|

Polysilicon |

10% |

Produced from metallurgical grade silicon, via trichlorosilane; used in manufacture of solar panels |

Figure 18‑2. The silicon metal value chain

Figure 18‑3. Applications of silicon metal1

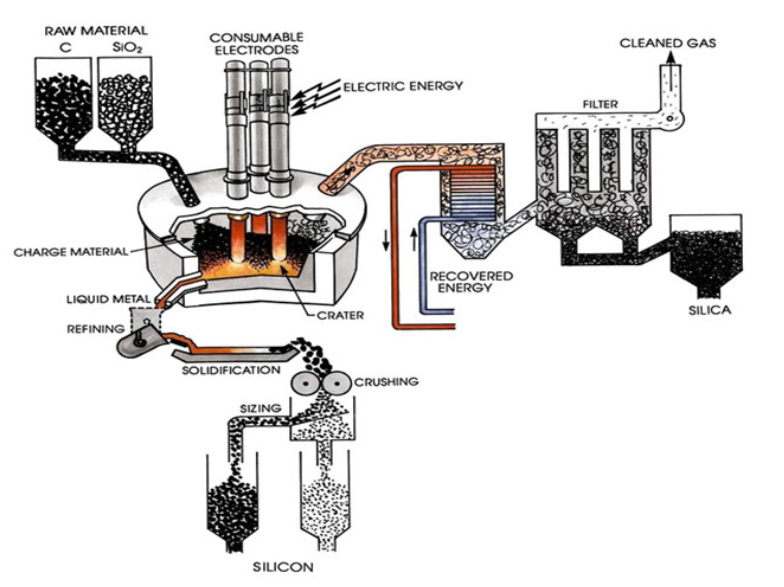

Production of silicon metal

To produce silicon metal, natural quartz in chunks of 3 to 15 cm is mixed with a source of carbon and heated to more than 2800°C to drive off the oxygen (Figure 18‑4). Note that silica sand cannot be used for silicon metal manufacture because the smaller particle size prevents adequate oxygen supply.

Figure 18‑4. Production of silicon metal

Substantial investment is needed to establish a silicon metal smelter. Silicon expert Mian Habib provides the following estimates of the inputs needed to produce 1 ton of silicon metal:

-

Inputs: Approx. 3 tons quartz, 1.5 ton low sulphur pet coke (carbon source)

-

Power: 11-13 MWh/ton electricity source

Quartz for production of silicon metal can be washed and sorted but further beneficiation is not possible (unlike production of HPQ, see Section 19), and therefore quartz for production of HPQ must meet the following purity specifications:

-

SiO2: 99-99.5%

-

Al <0.06%

-

Ca <0.06%

-

Ti <50ppm

-

Fe<0.1%

-

K<0.06%

-

P<0.001%

-

Na<0.01%

Mr Habib estimates that a greenfield silicon manufacturing plant normally produces 30,000 tons of silicon per year and costs about $350 million. He states that about 90,000 tons of quartz is needed to produce 30,000 tons silicon metal and concludes that about 2 million tons of quartz is needed for financial viability, which will support an investment for about 20 years.

The market opportunity for silicon metal

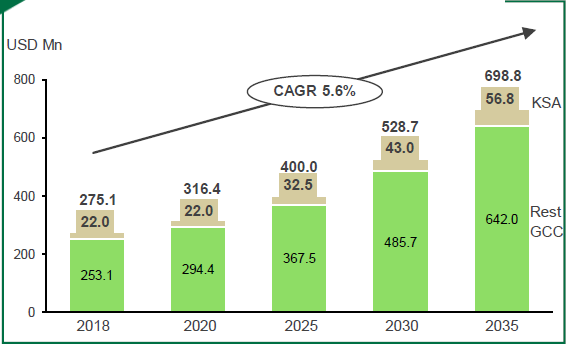

The global silicon metal market is projected to grow from $7.5 billion in 2020 to $9.7 billion by 2026, growing at a CAGR of 4.4%. Growth in the GCC region is estimated to be slightly above average: Figure 18‑5 shows the market size and projected growth across the GCC region1.

Figure 18‑5. Market size and projected growth for silicon metal across the GCC region405

Demand for silicon metal is met mainly by smelters operating in China, the USA, Iceland, and Malaysia. There appears to be a strong opportunity to establish a silicon smelter in the GCC because of lack of local production and lack of competition from any major player, global or local.

Market demand is driven by the following:

-

For aluminium production: growth in flat rolled products, extrusion, casting, and wire production.

-

For chemical silicones: demand is expected to rise due to increasing production of paints and coatings, surfactants, lubricants, sealants, adhesives, rubber, glass, ceramic, and foundry.

-

For polysilicon: demand is expected to rise due to expected growth in the solar energy and electronics industries (estimated CAGR of 6% over the next five years) – expected to be dominated by demand from Asia-Pacific countries, especially China and India, but government commitments to renewable energy are also expected to drive demand in the GCC.

Case study: Silicon metal smelter in Iceland

Iceland built an advanced and environmentally friendly silicon metal smelter in Husavik, which became operational in 20181. It has capacity to produce 32,000 metric tons of silicon metal per year. The smelter is owned by PCC BakkiSilicon and the raw quartzite is sourced primarily from PCC’s quarry in Zagorze, Poland. Although this source incurs logistics costs, these are outweighed by the advantages of Iceland’s geothermal and hydropower resources, which lead to favourable electricity costs. About 80% of silicon metal produced in Iceland is sold in Europe, especially Germany, with the rest sold to North America2. In July 2020, soft market prices caused PCC BakkiSilicon to cease production for an indefinite period because of weak market prices in both Europe and the USA. This is likely to be related to the pandemic and reports of the smelter operating again as the world starts to emerge from the pandemic have not been found.

Plans for silicon metal smelters in the GCC

Establishing a silicon metal smelter in the United Arab Emirates

In 2014, Silicon Metal of Abu Dhabi planned to build a silicon smelter in the Khalifa Port Industrial Zone, Taweelah, in the UAE, with planned production of 36,000 tons of silicon per year in the first instance, and potentially double that amount in the future1,2. However, no reports were found to suggest this smelter has been completed, and Saudi Arabia has published an investment opportunity that reports a lack of silicon smelters across the GCC, suggesting that the UAE smelter has not been established as planned.

Investment opportunity to establish a silicon smelter in Saudi Arabia

Saudi Arabia has recognised a high potential opportunity to invest in a silicon metal smelter given the lack of a smelter in the GCC region and published a summary of the opportunity in September 2020 with the aim of attracting investment.

Saudi Arabia currently imports silicon metal to meet local demand and imported 8 kilotons of silicon metal in 2018. A smelter would both cater to local demand and serve regional markets, with the geographical location and trade agreements with neighbouring countries expected to support potential exports. A strong advantage for Saudi Arabia is its competitive energy prices, which constitute about 45% of the operating costs of the smelter. The project will be enabled by governmental support, including:

-

Up to 75% of the project financed by the Saudi Industrial Development Fund (SIDF).

-

A 2-year grace period for the repayment of loans.

-

The Human Resources Development Fund, providing 30%, 20%, and 10% of Saudi nationals’ salaries for their first, second, and third years of work respectively.

Saudi Arabia has estimated the financial factors for the smelter:

-

Expected investment size of $140 million.

-

Plant capacity 45 ktpa.

-

Expected IRR: 14.1%.

-

Payback period: 9.2 years.

Opportunity for silicon smelter in Oman

Oman recognised the potential to set up a silicon metal smelter in 2015. Lou Parous, Executive Director of German engineering company Viridis.iQ1, which has expertise on every step of the silicon value chain, highlighted that Oman benefits from an estimated 4.5 million tons of quartz deposits in Saih Hatat. Oman also has low-cost electricity, competitive financing, and industrial infrastructure2. Parous commented that Oman’s Free Trade Agreement with the USA, which is one of the biggest consumers of metallurgical silicon, means it is an ideal location for a silicon smelter. As well as export opportunities, a domestic silicon industry can catalyse investment downstream industries in Oman (production of photovoltaic panels, silicones, and production of aluminium and metal alloys). Viridis.iQ supports both new and existing projects in both established and emerging markets and would be a strong potential partner for establishing and operating a smelter. However, these observations were made in 2015 and no evidence has been found of any recent developments in this area. One interviewee attributed the lack of activity to failure to attract investment, as well as lack of required technological know-how in Oman and lack of infrastructure and communications to build an industry and supply downstream industries3.

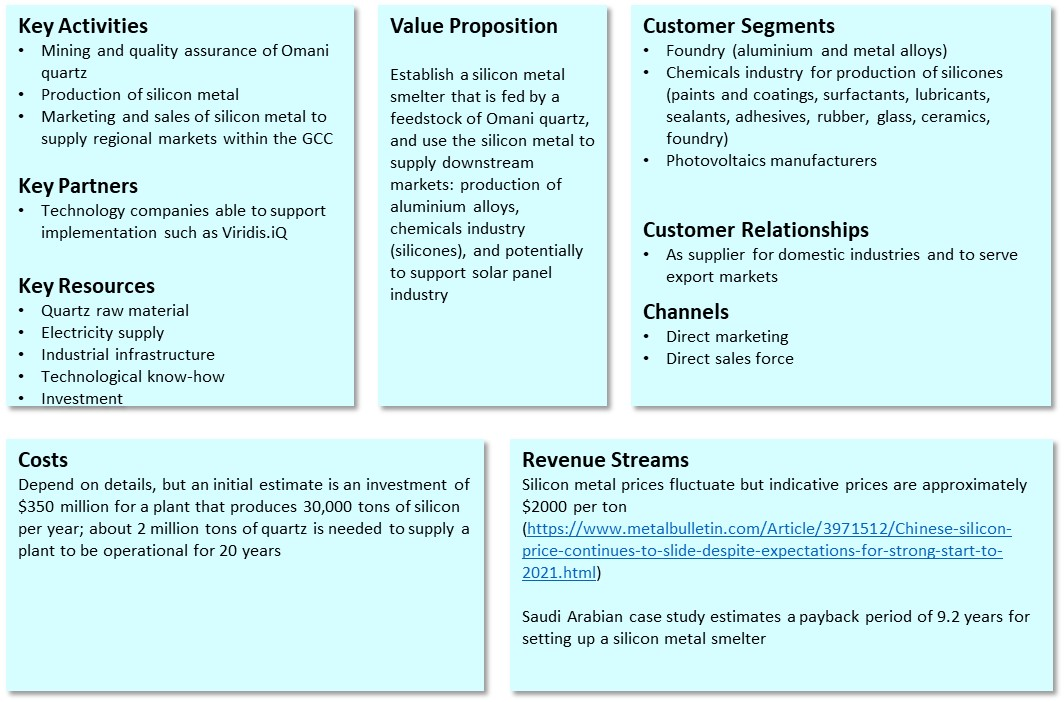

Business canvas

Figure 18‑6. Business canvas for establishing a silicon metal smelter in Oman

Next steps

Next steps towards establishing a smelter are as follows:

-

Characterize Omani quartz deposits and establish that reserves are of sufficient quality and quantity to supply a silicon metal smelter. Ensure that electricity can be supplied at an economically feasible price and establish the industrial infrastructure needed for a smelter to be successful.

-

Conduct a market study to determine the feasibility of establishing a supply of Omani silicon metal and to establish downstream markets to target, which are expected to be aluminium production, other alloys, and the chemicals industry (silicone production), as well as photovoltaic panels. Oman could supply regional markets within the GCC.

-

Seek investment and the technical expertise required to establish the smelter – Viridis.iQ is recommended as a strong potential partner.