Background

The term lime encompasses several types of product, all derived from limestone or calcium carbonate.

The main types are as follows:

• Quicklime (also called burnt lime or unslaked lime) is calcium oxide (CaO). It is a white, caustic, alkaline substance, produced via calcination in a lime kiln above 900°C. Theoretically, 56 kg of CaO is produced from 100 kg CaCO3 during complete calcination (or 1.8 tons of limestone needed to produce 1 ton of quicklime) but in practice, levels can vary1.

• Slaked lime (also called hydrated lime) is calcium hydroxide, Ca(OH)2, usually 72%-74% CaO with 23%-24% H2O

• Hydraulic lime is made from a limestone that either naturally contains some form of amorphous silica or has it added to the burning process; the amorphous silica fuses with some of the quicklime to form a clinker, a cementitious compound. Hydraulic lime comprises a relatively minor part of the lime market2.

• Other minor lime types are produced by calcination, including the following:

o Dolomitic quicklime (CaO+MgO)

o Dead burned dolomite (MgO)

o Type N dolomitic hydrate (Ca(OH)2+MgO)

o Type S dolomitic hydrate (Ca(OH)2+Mg(OH)2)

Production of lime

Following limestone mining, lime production requires crushing, screening, and grinding, followed by a calcining step. Figure 11-1 shows a summary of the process for producing different types of lime. The process includes a two-stage crushing process, followed by calcining (heating) in a lime kiln at over 1000°C, and summarizes the differences in production of quicklime, slaked lime, and hydraulic lime. All steps can cause significant pollution at a local level, and Table 11-1 summarizes best practice to minimize the generation of pollutants.

Production costs

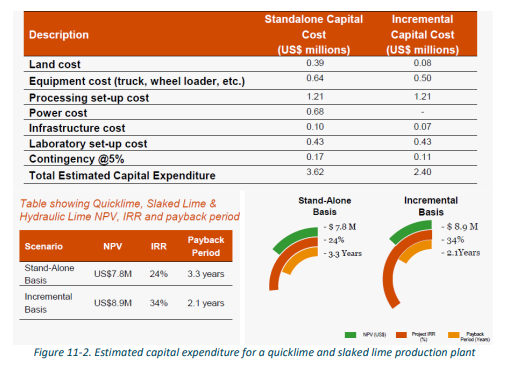

A 2019 study of the potential of the limestone industry in Jamaica concluded that an investment in developing quicklime, slaked lime, and hydraulic lime could be financially feasible for a total production of 29,285 tonnes per annum. This analysis examined two scenarios: a standalone (startup) basis, and an incremental basis, i.e. adding GCC production on to an existing operation. On an indicative basis, the internal rate of return was calculated to range from 24.0% to 34.0%, and net present value (NPV) to range from $7.8 million (for standalone basis) to $8.9 million (for incremental basis).

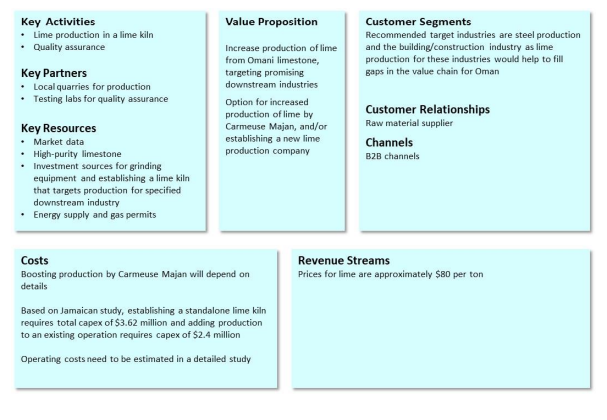

The case study estimates a total capital expenditure of $3.62 million to set up a standalone lime production plant, and $2.40 million to add lime production to an existing operation. Some costs, notably equipment costs, laboratory costs, and infrastructure costs, are based on industry standard figures and provide a reasonable starting point for estimated costs in Oman. However, cost of land, power, and cost of transporting equipment are based on Jamaica, and may differ significantly in Oman. The notes in Figure 11-2 indicate the source of the estimates and comment on expected similarities or differences in Oman. Note that the case study also includes detailed estimates of operating expenditure, but these are not included in this report as they are likely to vary substantially in different geographic regions.

Notes:

Land: Based on cost per hectare of land in Jamaica (estimated at $30,000 per hectare). Estimated that one hectare of additional land is needed in addition to an existing quarry for production of lime, including plant facility, workshop, storage area, waste disposal, worker camps, etc.

Equipment: Calculated based on cost of truck and wheel loader sourced from the USA with contingencies added to cover for transportation and duties for Jamaica.

Processing set-up: Includes crushing, screening, grinding, kiln and hydration processing and systems, and supporting plant equipment, sourced from China (because of lower procurement costs). Also assumes semi-mechanised packaging facility due to the very fine mesh size of the ground limestone which is not suitable for manual packaging. These aspects are likely to be very similar for Oman. However, the figures include transportation and duties that were estimated for Jamaica.

Power: Assumes power provided from grid and that a grid connection is already established.

Infrastructure: Includes covering shed, laboratory facilities, etc. and is based on typical industry standard costs for setting up value-added plants, therefore likely to be similar in Oman.

Laboratory set-up: Estimated for testing basic mineral content and size, for basic grade testing; estimate based on industry standard cost for basic laboratory testing equipment so likely to be similar in Oman.

Contingency: A 5% contingency is added to the total capital cost to cover project threats or uncertainties.

Downstream markets for lime

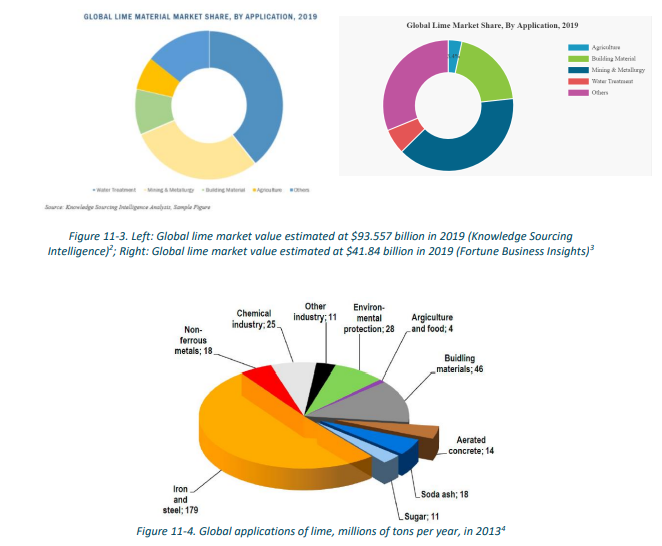

Lime is widely used across many industry sectors. The two largest applications globally are metallurgy and construction/building materials, and demand for lime in these sectors is expected to grow. Regarding metallurgy, lime is used to remove impurities during steel manufacture, and demand for steel therefore in turn significantly influences demand for lime1. Demand for steel and other metals from automotive and other manufacturing industries comes from across the globe but is especially strong in developing economies such as China, India, and Brazil. The World Steel Association forecasts that steel demand will grow by 5.8% in 2021 to reach 1.874 billion mt, after declining by 0.2% in 20202. Demand for lime from the construction industry is also expected to grow as construction increases globally1. The growth is expected to be especially high in developing economies, such as China, India, and countries in GCC, where construction is backed by rising private and public investments. Other applications of lime include environmental/water treatment, agriculture, food production, chemicals industry, etc. (Figure 11-4).

Opportunities for lime production in Oman

Table 11-2 summarizes the use of lime in various downstream applications and considers the possible opportunity for Oman

Production of lime in Oman

Carmeuse Majan is the only international company with lime operations in Oman. Based in Salalah Free Zone, in 2018 it produced 400 tonnes of lime per day with one kiln1. The company now has four kilns in operation. Carmeuse supplies the Oman market and other neighbouring countries, with most of its product exported to India. India is a major export market for Omani lime. Local production of lime in India is constrained by poor resources, a non-ideal source of limestone in Rajasthan, and poor transport infrastructure2. India consumes a very high quantity of lime for its steel industry and is aiming to grow the industry to produce 300 million tonnes of steel annually by 2025 to 2030. Production costs for lime in Oman are therefore lower than local Indian production, increasing the attractiveness of Omani lime. Carmeuse initially aimed to build up to eight kilns over the next 10 to 15 years but has since reduced this aim as the company experienced issues with gas allocation for the kilns. Additionally, an interviewee from Kunooz Holdings (an associate company of Carmeuse Majan) suggested that the Indian market had not grown as much as had been expected3.

The second lime-producing company in Oman is CMI, in the north of Oman, with its main plant in Quriyat4. This company has two production plants and exports mainly to the UAE and GCC steel industries as well as to India and Africa. CMI has plans to extend their hydration plant facilities.

Challenges for the Omani lime industry

Carmeuse Majan outlined challenges facing the Omani lime industry:

• Energy-related – issues over obtaining gas permits and the high cost of energy.

• Environmental issues – the challenge of high emissions and the need to progress towards becoming carbon neutral.

• Infrastructure related – challenge of attracting foreign investment to develop the lime industry: Section Error! Reference source not found. reviews this topic and discusses recommendations.

• Market issues: A limited domestic market for lime (see Section 11.4.1).

Energy-related issues

Carmeuse Majan described severe struggles in the past with obtaining gas permits. While this has eased to some extent, the industry still faces uncertainty and challenges created by the terms of the gas permit contracts, which tie the price of gas into the percentage of Omanisation required from any company that uses gas. Carmeuse Majan commented that current Omanisation targets set by the Omani government constrain productivity because young people are more attracted to office work or to the finance sector than to heavy industry1.

Carmeuse Majan recommended the following steps:

• Increase flexibility and pragmatism when setting Omanisation policies, taking into account industry conditions, and adapting targets so that they are realistic for each industry.

• Target education in Oman to meet the needs of the market. Stronger technical education is needed at school level to boost interest in industry and raise enthusiasm for working in it later.

Environmental issues

Lime production is highly energy intensive, with electricity and fuel costs potentially comprising 40 to 50 percent of total production costs. The industry is therefore vulnerable to increases in fuel prices2. The high energy demand also raises environmental issues. The environmental imperative to reduce carbon emissions from the lime industry is strong and European lime and cement industries have committed to becoming carbon neutral by 2050. Experts commented that few cement or lime plants have achieved this status as yet, so not being carbon neutral is unlikely to put the Omani lime industry at a disadvantage in the world markets today. However, the Middle East is in general significantly behind Europe in this regard, and experts bel ieved that to become world class, Omani companies need to demonstrate progress towards this goal3,4. All companies need to balance their environmental imperatives with making a profit. However, the changes required are on a huge scale and the issue needs to be tackled at an industry level through conversations between government and industry to create a new energy strategy for the country that supports the lime industry and other industries that have high energy consumption.

As a global lime enterprise, Carmeuse has a separate company handling initiatives in reducing CO2 emissions and CO2 capture, potentially for resale. A brief summary of steps that Omani lime companies can adopt to move towards being carbon neutral is below (further information is available from the EU Lime Association) 5:

• Maximise solar energy for electricity generation for lime plants and watch technology developments in the use of solar power to heat the kiln; in the future, high-temperature Central Receiver Systems (CRS) with pressurised air could reach achieve kiln temperatures up to 1000°C.

• Consider switching from horizontal kilns to vertical kilns, which, depending on the type of operation, can increase energy efficiency1.

• Improve the use of waste heat from the kilns and from hydrated lime production. Waste heat can be used to dry or preheat the limestone, in limestone milling, or to generate electricity. It can also be channelled to supply heat for other industrial processes such as in the food and drink or chemical industries, should operations be located near the lime plant.

• Consider the use of alternative fuels with lower carbon energy sources.

• Carbon capture and storage – these technologies are currently still expensive but the prices are expected to fall in response to global legislation changes to support techniques. A precipitated calcium carbonate (PCC) plant would be one option to reuse CO2 emissions from lime production (see Section 10.6.1).

Limited domestic market for lime

Although there are many applications for lime, the small size of downstream Omani industries means that only small volumes can be used domestically. Carmeuse Majan recommended that to build the domestic market for lime, the focus should be on opportunities for lime that would fill gaps in the value chain in existing Omani industries. This requires detailed market opportunity studies for potentially viable industries, which would consider sources and availability of raw materials, barriers to entry in the market, logistics issues (shipping, customs, etc.), the size of the investment needed, etc. Once downstream industries with high potential have been identified, the next step will be to attract foreign investment. Government support will be needed to offer appropriate incentive packages and to streamline the bureaucracy associated with investing in Omani industry (see Section Error! Reference source not found.). This rationale underlies the decision by Carmeuse Majan to focus on lime production to support the steel industry. The analysis in Table 11-2 suggests that the most promising opportunities for lime are production for the steel and for the building/construction industry. Smaller scale or longer term opportunities may be to supply non-ferrous metallurgical applications, the chemicals industry, production of soda ash for glassmaking, and possibly the food and beverage industry.

Business canvas

Next steps

The next step for boosting the Omani lime industry is to continue to work with Carmeuse Majan to help to overcome the challenges they described. Carmeuse Majan emphasized the constraints brought upon production by the current policies that tie usage of gas with meeting Omanisation targets and suggested that greater flexibility in this regard would significantly help the industry. Also, the Omani government could support the lime industry and other energy-intensive industries by adjusting policy to support environmental initiatives that will help to lower the carbon footprint of lime production. In parallel, a detailed market study should be performed to evaluate the potential of different downstream markets and to understand the level of production needed to meet expected demands. The outcome of such a study can be used to determine if investment into further lime production facilities would be worthwhile.